April, 2, 2026 - In line with the full-year forecasts published towards the end of last year, the Amaplast Study Center - a trade association affiliated with CONFINDUSTRIA that brings together over 170 manufacturers - estimates that the Italian industry of machinery, equipment, and moulds for plastics and rubber closed the year 2025 with a decrease in production on the order of five percentage points, and with a value of 4.4 billion euros. This represents a slowdown with respect to the previous year, 2024, where a limited deceleration was recorded. For comparison, the Germans – the Italians’ direct competitors – in 2024 had already begun recording a significant slump in orders, sales, and exports. Italian exports for the sector, which account for three quarters of production, also recorded a drop of 5%, coming in at just barely over 3.4 billion euros.

With respect to the weakness in sales abroad, imports of technology recorded a surge of nearly twenty-four percentage points over 2024, confirming robust domestic demand. This is clearly due partially to the effects of the incentives implemented by the Industry 4.0 and 5.0 Plans, in spite of difficulties in accessing them and delays in the enactment of the various associated implementation decrees. These issues are also critical in this first quarter of 2026 in the implementation of measures regarding the new “hyper-amortization” of investments in capital equipment through September 2028.

Given these dynamics, the balance of trade is significantly reduced: after the record of 2.65 billion reached in 2024, it has slipped back to 2.24 billion.

The international context in 2025 was characterized principally by uncertainties caused by the introduction of tariffs by the Trump administration which, beyond the “reciprocal” component, raise the tariffs on steel and aluminium components in certain types of machinery, components, and moulds for plastics and rubber.

The situation was worsened by the progressive devaluation of the dollar with respect to the euro. It deteriorated further with the outbreak of the troubling war in the Middle East, which has triggered an energy crisis that has already begun to have a strong negative impact on the European plastics and rubber processing industry by increasing the costs of natural gas, petroleum, and raw materials and generating uncertainties about the availability of materials.

This situation is the source of significant concern among Italian manufacturers of plastics and rubber processing machinery, with a host of factors that threaten to compromise the propensity for investment in the domestic market – here understood as both the Italian and the European market, the latter historically the main destination for Italian exports – and challenges in store with the implementation of the new European Packaging and Packaging Waste Regulation (PPWR).

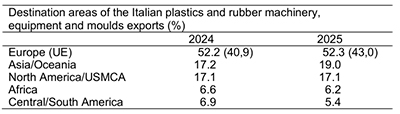

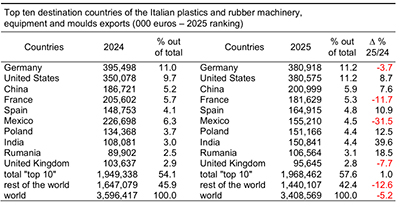

Not surprisingly, sales to Germany, which has always been Italy’s prime trade partner, have fallen for the second consecutive year. The German plastics and rubber industry recorded losses across the board in 2025 according to estimates by various trade associations: -4% by volume in polymer production; -2% of processed plastic products; -6% for rubber products; and -5% in revenues for machinery manufacturers.

Exports to processors in France, another major export destination in the EU, have also fallen off. Within the top ten destination markets, these negative trends have fortunately been compensated by an increase in sales to Spain, Poland, and Romania.

On the other hand, as of last December, the abovementioned issues have not yet caused the feared collapse of Italian exports to the American market. Instead we have witnessed an increase of almost nine percentage points. U.S. domestic machinery production meets only a limited share of local demand and so American plastics and rubber processors have continued to turn to Italian and other manufacturers to acquire advanced technology.

Sales to China have continued to increase at a steady pace but those to India even more so, more than tripling in the past ten years: the growing incentives provided by the Make in India programme have generated a strong acceleration of demand by local manufacturers, who require increasingly high quality technological systems. So this is a market with notable potentials, most of which have yet to be developed. The recently signed free trade agreement should facilitate this process.

On the other hand, two other important countries that recently rejoined the group of top ten destination markets have produced disappointing results for Italian manufacturers: sales to Turkey have plunged by one third, breaking a five-year robust growth trend, and those to Brazil performed even worse, -45%, although this is relative to the abnormally high peak in 2024 and actually represents a return to the average figures recorded in the previous period. We are naturally looking forward to the implementation of the EU-Mercosur treaty, which could inject new dynamism into trade with Brazil and South America generally.

As regards product categories, exports overall have shown lacklustre or diminishing performance for most of the machinery types accounting for the largest share of the total, starting with extruders (falling from nearly 400 to 350 million euros), blow-moulding machines (from 212 to 198 million), flexography machines (from 181 to 164 million), and moulds (from 752 to 721 million). Injection moulding machines were the only ones to buck the trend, with sales rising from 194 to 199 million. In this complex situation, Amaplast member companies finished the year 2025 with a downturn in revenues on the order of five percentage points while nevertheless succeeding in maintaining

employment levels (+0.5%). Within this group, 54% of the companies closed the year with a drop in sales.

It has never been so difficult to venture forecasts for the coming months: there are too many unknowns that continue to arrive and overlap on the international level, aggravating the climate of uncertainty that companies are facing, with many historical destination markets characterized by greater difficulty of access.

There will be an opportunity for discussion and updates among international operators in the plastics and rubber industry this year at PLAST 2026 in Milan (9-12 June), organized by Promaplast srl, the Amaplast service company.

As the exhibition slowly takes shape – with over 160 new participants with respect to the previous edition, 30% of them foreign companies – the organization of associated events and the reception of hundreds of qualified buyers is well underway, in collaboration with Agenzia ICE and the principal foreign manufacturers associations.